Build credit products you actually own.

Embedded finance platforms take your margin and own your customer relationships. Liftline gives you direct access to lenders and insurance, plus the software, AI agents, and expertise to make it effortless — so the economics scale with you, not against you.

The embedded finance trap.

What they tell you

"Launch in weeks"

What they actually mean

Lock-in for years

Fast onboarding hides long-term contracts and integration dependencies. Switching costs are the product.

What they tell you

"We handle everything"

What they actually mean

We own everything

They own the lender relationship, the insurance policy, the customer data, and the underwriting decisions. You own a revenue share.

What they tell you

"Revenue share"

What they actually mean

They keep the spread

You get a thin slice. They keep the lender economics, the insurance margin, and the platform fee. As you scale, their margin expands instead of yours.

What they tell you

"No balance sheet risk"

What they actually mean

No balance sheet upside

They derisk you, but they also cap your economics. You'll never build equity in your own capital program.

The math your embedded finance provider hopes you won't do.

$10M/month in funded receivables

With an embedded finance platform

They source the lender

They set the advance rate and cost of capital.

They buy the insurance

They control the coverage and margin.

You get a revenue share

Typically 30-50% of the net spread.

Your spread: ~$45K/month

With Liftline (direct relationships)

You have the lender relationship

You negotiate your own terms and advance rates.

You hold the insurance policy

You control coverage and cost.

You keep the full spread

Minus Liftline's infrastructure fee.

Your spread: ~$105K/month

Same receivables. Same customers. Dramatically different economics — because you own the relationships that matter.

The infrastructure layer to own your capital stack.

Liftline sits between your platform and institutional capital, giving you everything you need to build and run credit products — without the middleman.

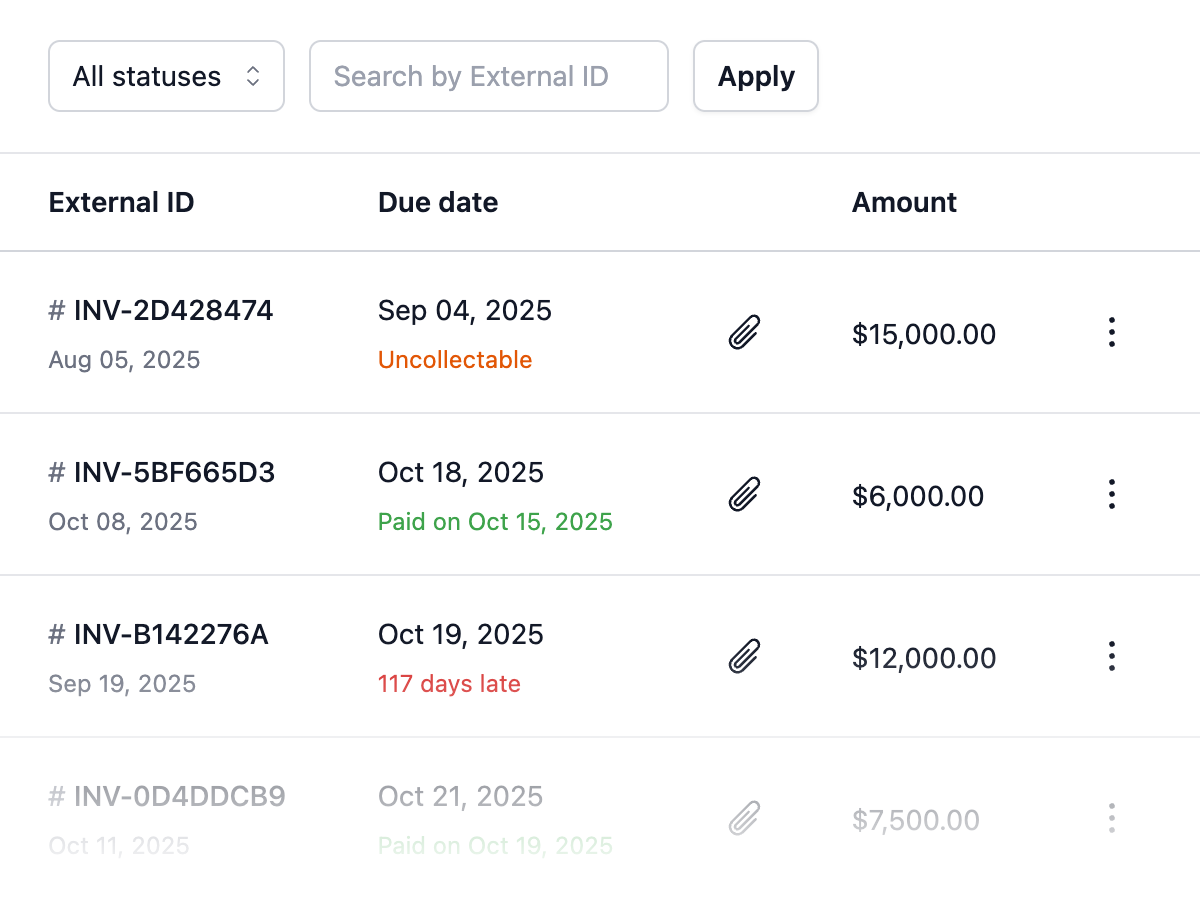

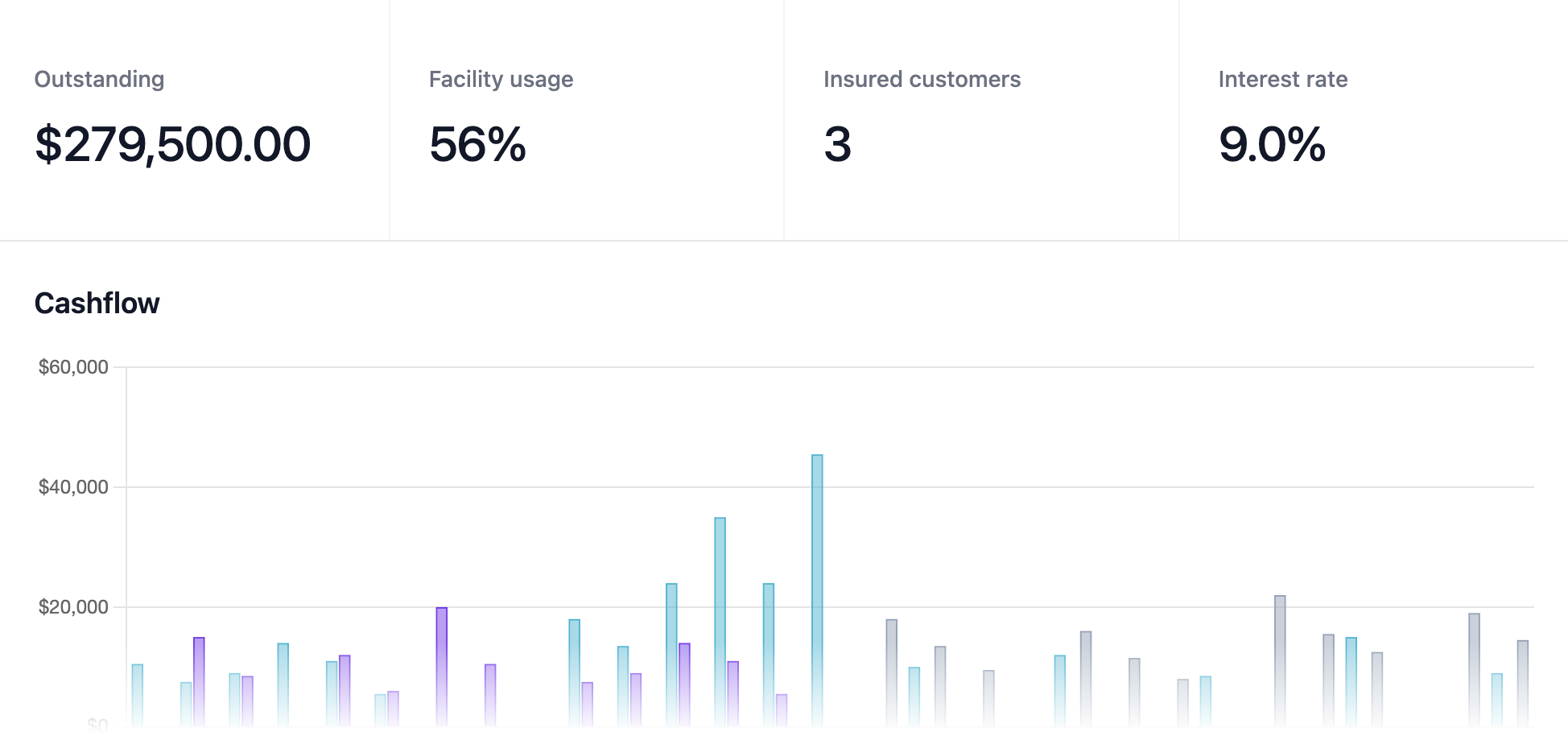

Receivables Transformation

Turn your AR into insured, lender-ready assets

Liftline uses trade credit insurance to derisk your accounts receivable for lender underwriting. You hold the policy directly.

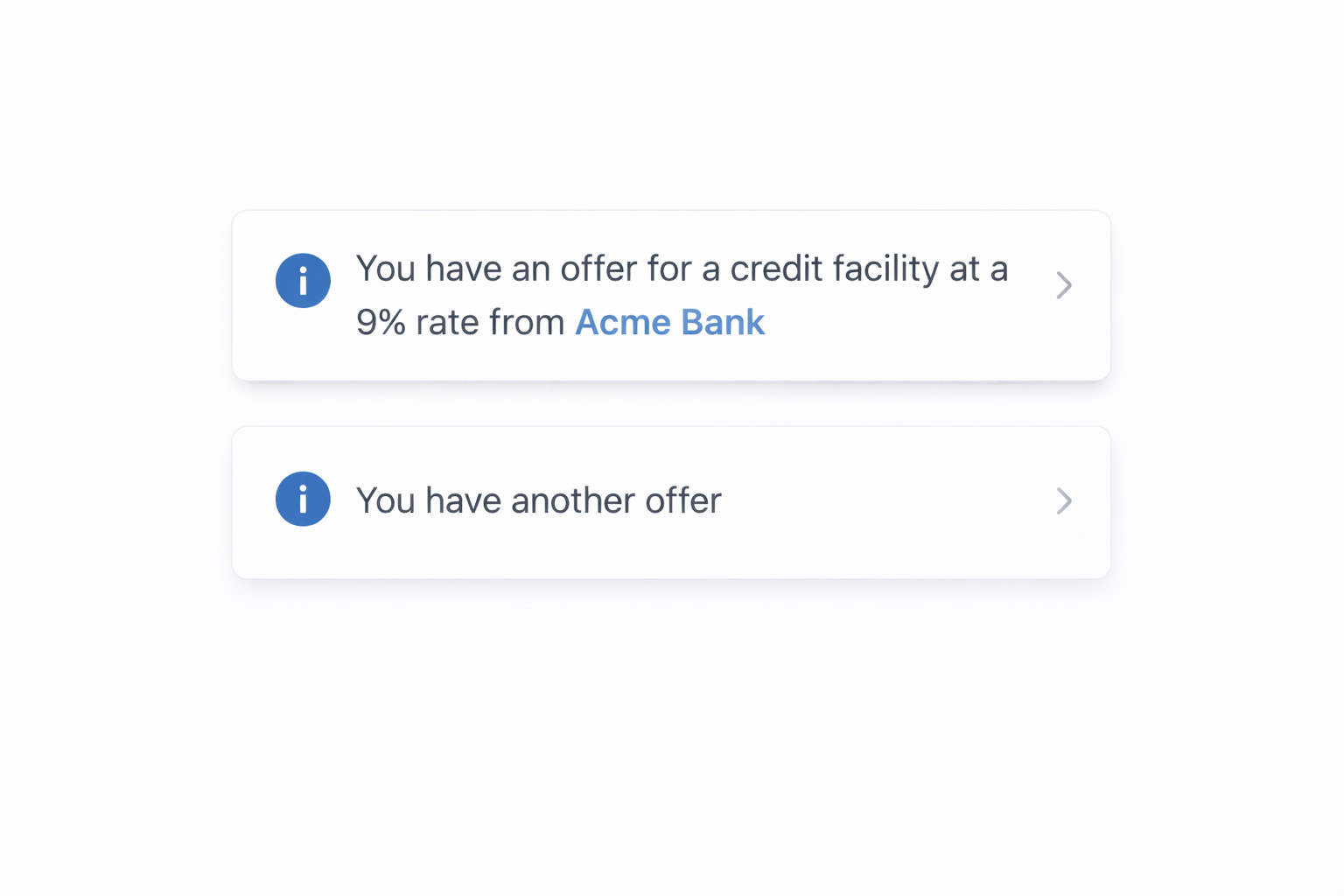

Direct Capital Access

Your lender relationships, your terms

We connect you with institutional lenders. You own the relationship, negotiate your own terms, and keep the economics.

Structuring

Legal and account structures, built to deploy

From on-balance-sheet setups to off-balance-sheet SPVs. Pre-built frameworks designed to support financing without disrupting existing agreements.

Software & AI

Dashboard, APIs, and AI agents

Manage eligibility, limits, performance, and lender-approved reporting with a modern platform built for scale.

Expert Guidance

Scaled fintech to billions — now we scale yours

Our team works alongside you to design, launch, and iterate on credit products, informed by experience scaling fintech offerings to billions of dollars of volume.

From zero to live in weeks.

1

Tell us what you want to build

Net terms? Payment acceleration? BNPL? We'll help you design the right product for your customers.

2

We set up the infrastructure

Lender introductions, insurance placement, legal structures, bank accounts. All in your name.

3

Integrate with your platform

Use our fully white-labeled portal to give your customers an out-of-the-box experience under your brand, or build a fully custom integration with our APIs. Either way, you're live fast.

4

You own the product

Your brand, your customer relationships, your economics. We provide the rails.

What platforms are building with Liftline.

-

Before LiftlineA two-sided marketplace had 90-day payment terms from buyers but a 30-day payment obligation to suppliers. The mismatch resulted in cash flow constraints & limited growth.With LiftlineBy converting invoices into receivables-backed capital, the marketplace rolled out a supplier payment acceleration product — creating a new revenue stream while improving supplier liquidity. They own the lender relationship and keep the full economics.

-

Before LiftlineA SaaS platform for subcontractors had demands to offer net terms greater than 30 days. Balance sheet constraints made this impractical, resulting in decreased usage and off-platform transactions.With LiftlineThe platform offers extended net terms funded by receivables-backed capital — improving customer retention, increasing platform usage, and unlocking incremental revenue. No embedded finance middleman taking a cut.

-

Before LiftlineCustomers wanted flexible payment options, but offering installment-based terms required underwriting credit and tying up operating cash — neither fit the business model.With LiftlineThey built a B2B BNPL product backed by insured receivables. Customers pay over time, the platform maintains predictable cash flow, and the economics are theirs — not a third-party platform's.

-

Before LiftlineA PE-backed rollup was acquiring companies across a fragmented industry. Each entity had its own inefficient factoring arrangement — different providers, different rates, different contracts. The cost and complexity were dragging on margins.With LiftlineThe rollup consolidated all entities onto a single Liftline-powered factoring program with unified lender and insurance relationships. Better rates at scale, one dashboard across the portfolio, and freed-up cash flow that accelerated both growth and profitability.

Stop renting your capital program. Own it.

Liftline gives platforms direct access to the lenders, insurance, and infrastructure to build credit products with economics that scale.